The Post-Omnibus Era

The New Simplified ESRS Datapoints Are Locked In

The regulatory framework for corporate sustainability in the EU has reached a major milestone. On May 6, 2026 the European Commission published the draft revised European Sustainability Reporting Standards (ESRS), incorporating the simplifications introduced by the Omnibus I legislative package. Following the closure of the public consultation period on June 3, 2026, the updated framework is now being finalized. This transition marks the beginning of the post-Omnibus era, a regulatory shift designed to ease the administrative reporting burden on European businesses while maintaining high-quality disclosure standards.

What Does the Easing Mean for Businesses?

The primary goal of the post-Omnibus package is to streamline compliance by removing redundant or highly complex requirements. The key structural changes include:

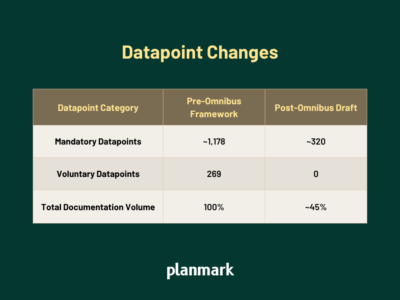

- A 61% Reduction in Mandatory Datapoints: The number of required “shall” datapoints (subject to materiality) has been reduced from approximately 1,178 to ~320.

- Complete Removal of Voluntary Disclosures: All 269 voluntary “may” datapoints have been completely deleted from the standards.

- The “Shall Not” Over-Report Rule: Previously, many companies over-reported non-material data due to cautious auditing interpretations. The wording in ESRS 1 has been hardened to state that undertakings “shall not” report non-material information, establishing materiality as a strict filter.

- Top-Down Double Materiality Assessment: Rather than conducting a detailed assessment of every individual impact, risk, or opportunity (IRO), companies are now permitted to apply a “top-down” approach, drawing materiality conclusions at the broader topical level.

- Statutory Value Chain Cap: To protect smaller businesses, the regulations implement a strict value chain cap. In-scope enterprises are legally prohibited from demanding ESG data from value-chain partners with 1,000 or fewer employees that exceeds the voluntary reporting standard.

Technical Deconstruction of Topical Simplifications

To help corporate reporting teams align their metrics, the May 2026 revised draft introduces specific technical reliefs across individual topical standards:

- ESRS E1 (Climate Change): The draft standards introduce greater operational flexibility by allowing companies to choose between the financial control approach and the operational control approach for greenhouse gas (GHG) reporting. This directly aligns the ESRS boundaries with the Greenhouse Gas Protocol and IFRS S2, avoiding duplicate accounting efforts.

- ESRS E2 (Pollution): Reporting obligations for microplastics are now strictly limited to primary microplastics (those intentionally manufactured or added to products). The requirement to report on secondary microplastics (the breakdown of larger plastics in the value chain) has been removed due to measurement infeasibility.

- ESRS E3 (Water & Marine Resources): Disaggregation requirements are simplified, focusing metrics primarily on total water consumption, withdrawal, and discharge, with a specific focus on areas facing high water stress.

- ESRS G1 (Business Conduct): The governance standard has been restructured to align directly with the Policies, Actions, and Targets (PAT) model. Overlapping disclosures have been removed, and specific administrative indicators, such as average payment terms, have been deleted unless they are deemed highly material to the supply chain.

Transition Timelines and Phase-In Provisions

The May 2026 draft delegated acts distinguish transition timelines based on whether an undertaking is classified as a “wave-one undertaking” (entities reporting for financial years starting between January 1, 2024, and December 31, 2026) or “other undertakings” starting later. Understanding these tiers is essential for planning compliance resource allocation:

- Larger Wave-One Undertakings (Exceeding EUR 450 million net turnover and 1,000 employees): These entities must report on most material topical standards from their first year. However, they are permitted to omit certain topical standards—specifically ESRS E4 (Biodiversity and ecosystems), ESRS S2 (Workers in the value chain), ESRS S3 (Affected communities), and ESRS S4 (Consumers and end-users).

- Smaller Wave-One Undertakings (Not exceeding the EUR 450 million net turnover and 1,000 employees thresholds): These entities receive a much broader transition relief. They are permitted to completely omit all topical standards until financial year 2027, meaning they only need to report on the cross-cutting standards (ESRS 1 and ESRS 2 General Disclosures) during this transition period.

- Shared Phase-Ins: Both tiers of wave-one undertakings share the same phase-in timelines for quantitative anticipated financial effects (which are deferred until financial year 2030).

- Other Undertakings (Starting reporting on or after January 1, 2027): These entities are permitted to omit the E4, S2, S3, and S4 topical standards for their first two reporting years.

Planmark’s Platform Already Supports the Simplified Framework

While many organizations are currently analyzing how to transition their systems, our platform has already completed the technical transition. Because our platform operates with an automated regulatory library, the newly revised, simplified ESRS datapoints are active and ready for use.

The draft delegated acts are scheduled to apply generally from the 2027 financial year, but they include an option for voluntary early application in the 2026 financial year. By utilizing Planmark, proactive organizations can adopt the simplified, lighter compliance load for their current reporting cycle, bypassing the complex requirements of the original 2023 standards.

Strategic Implementation

The post-Omnibus framework represents a practical stabilization of corporate ESG reporting. While the volume of mandatory datapoints has decreased, the requirements for data accuracy and external audit readiness remain strict. Moving from manual, fragmented spreadsheets to an integrated data management platform ensures that compliance teams can focus on strategic improvements rather than manual administrative tasks.

To support companies transitioning to the simplified framework, Planmark offers a free 30-day pilot program. Organizations can upload their raw data, explore the updated platform, and generate a draft compliance report aligned with the newly simplified ESRS requirements.